Amiculum Blog Article

Navigating the new ‘most-favoured nation’ (MFN) reality: are pharma companies ready?

Navigating the new ‘most-favoured nation’ (MFN) reality: are pharma companies ready?

Navigating the new ‘most-favoured nation’ (MFN) reality: are pharma companies ready?

Navigating the new ‘most-favoured nation’ (MFN) reality: are pharma companies ready?

MFN is reshaping global pricing and access, with early signals of price spillovers, launch delays and reforms to pricing and reimbursement systems in ex-US markets. As a result, pharma companies are already seeing impact on global pricing architecture, traditional launch positioning and patient access delays as MFN models progress. At Amiculum, we recognize MFN as a central catalyst for market access change in 2026 and beyond. This is why we have examined current MFN trends and outlined how organizations can prepare for the changes ahead.

MFN has developed into a policy framework comprising three distinct models, GENEROUS (Generating Cost Reductions for US Medicaid), GLOBE (Global Benchmark for Efficient Drug Pricing) and GUARD (Guarding US Medicare Against Rising Drug Costs). GENEROUS is a voluntary MFN model for manufacturers participating in Medicaid in response to tariff threats presently developing. GLOBE (Medicare Part B) and GUARD (Medicare Part D) are proposed mandatory MFN models for manufacturers not covered by GENEROUS agreements, expected from October 2026 and January 2027, respectively.

Currently, 16 MFN agreements established under the GENEROUS framework have been announced between the US administration and pharmaceutical manufacturers. Under the proposed GENEROUS model, prices are benchmarked to the second‑lowest net price (adjusted for GDP per capita using purchasing power parity) across eight comparator markets: Canada, Denmark, France, Germany, Italy, Japan, Switzerland and the UK.

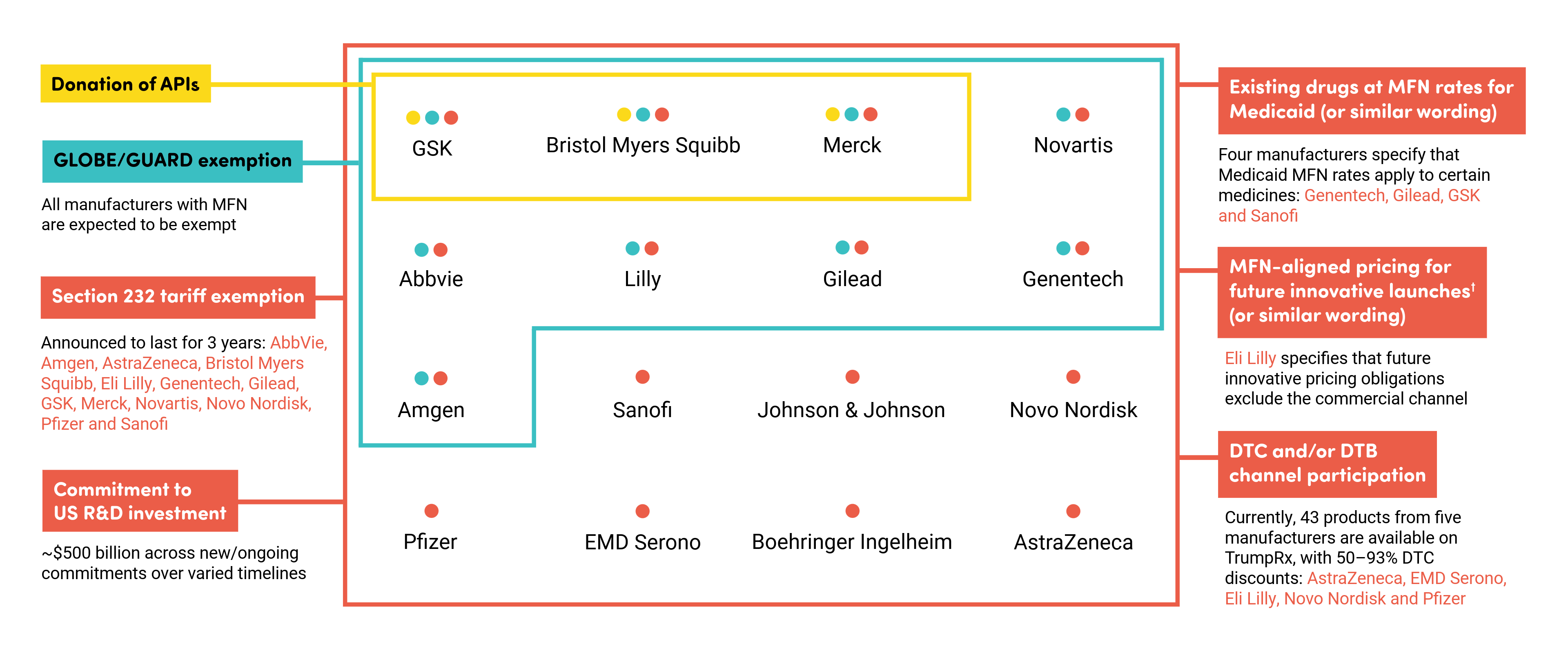

Key components of MFN agreements announced to date

Across publicly available White House and manufacturer statements to date, the key MFN (GENEROUS) deal components are broadly aligned with the US administration’s core requirements, although wording and scope vary (Figure 1).

Figure 1. MFN deal mapping – announced commitments and exemptions*

*The information in this figure is based solely on publicly available White House and manufacturer press releases. Many details remain confidential; therefore, some elements of the table may not fully reflect actual arrangements; †While Johnson & Johnson statements do not explicitly specify future launch commitments, they confirm that “the joint agreement meets the requests laid out by President Trump to the industry”. API, active pharmaceutical ingredient; DTB, direct to business; DTC, direct to consumer; GLOBE, Global Benchmark for Efficient Drug Pricing; GUARD, Guarding US Medicare Against Rising Drug Costs; MFN, most-favoured nation; R&D, research and development

Voluntary MFN participation under the GENEROUS model is expected to expand beyond the initial cohort from April 2026.

MFN spillover effects

A defining feature of MFN is the expectation that manufacturers will rebalance global pricing strategies and repatriate foreign revenue by negotiating higher prices in ex-US markets. Early evidence shows that this dynamic is already influencing both ex-US pricing posture and launch decision making across multiple markets among MFN-deal companies, with variations in how manufacturers are repositioning.

Pricing signals

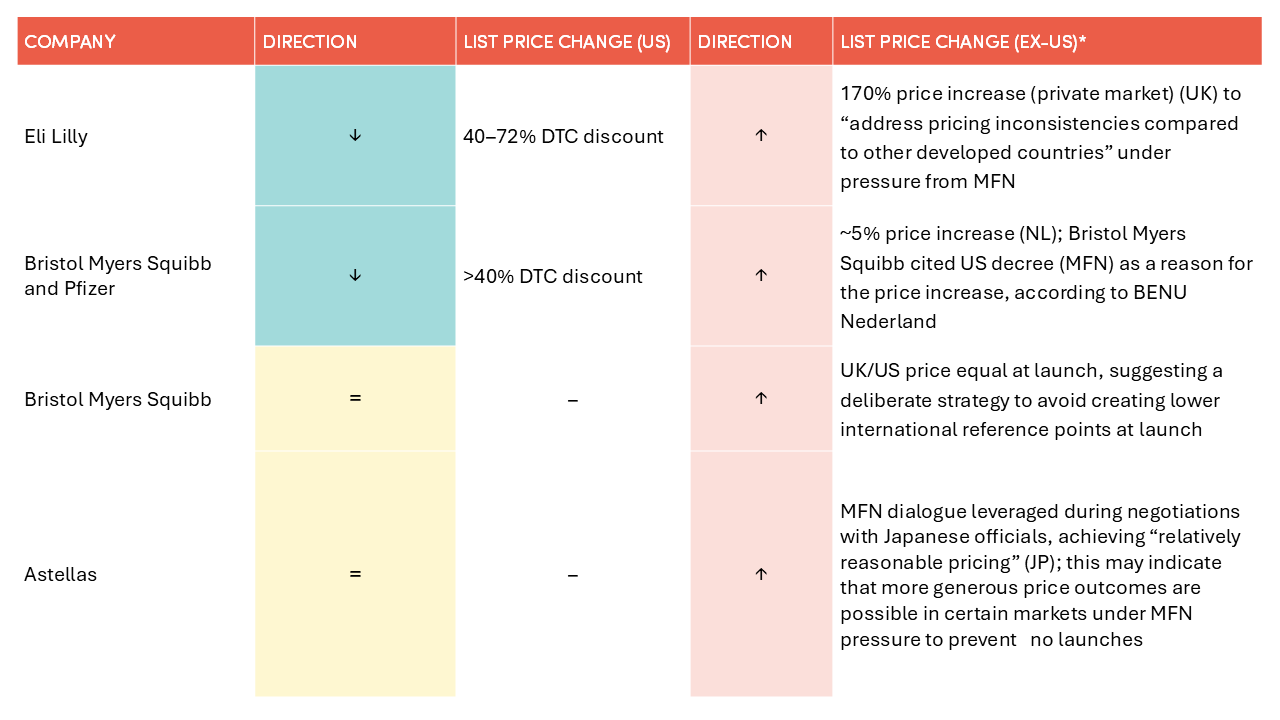

Early evidence indicates consistent US list price reductions or protections, often alongside increased list prices in ex‑US, MFN-referenced markets (Table 1).

Table 1. Illustrative examples of spillover effects on pricing strategies from MFN-deal companies

Each example represents a single product from the named company. *Actual increase or potential increase versus what would otherwise be possible without MFN pressure. DTC, direct to consumer; JP, Japan; MFN, most-favoured nation; NL, Netherlands

Launch timing and access implications

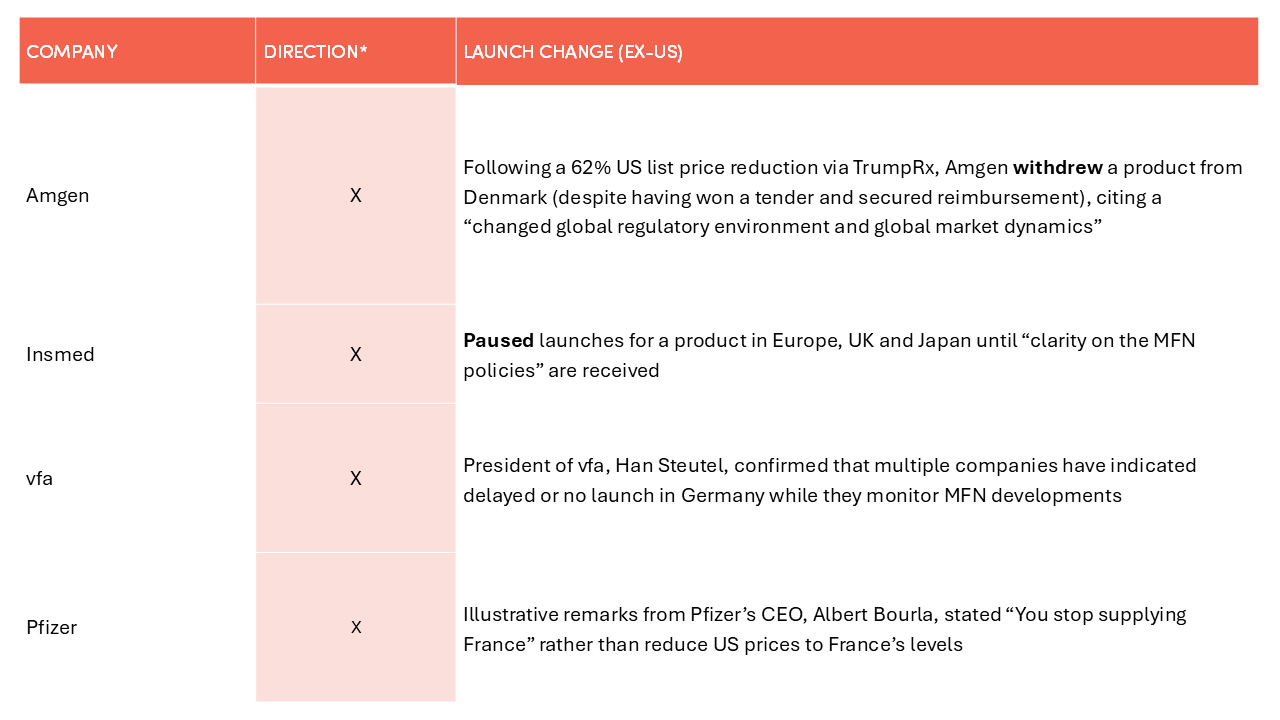

Across markets and indications, we are observing delayed and withdrawn launches in MFN‑referenced markets, particularly as manufacturers await greater clarity on the final MFN deal parameters (Table 2).

Table 2. Illustrative examples of spillover effects on launch strategy from MFN pressure

*Crosses represent no/withdrawn or delayed launch. CEO, chief executive officer; MFN, most-favoured nation; UK, United Kingdom; US, United States; vfa, Verband der forschenden Pharma‑Unternehmen

These decisions underscore the growing reality that launch prioritization and order will become a critical strategic lever in an MFN environment.

Market adaptation: UK policy reforms

Some markets are already adapting structurally to remain attractive under MFN pressure. To avoid US tariffs and support the US–UK post‑Brexit trade deal, the UK government committed to increase overall medicines spending and the National Institute for Health and Care Excellence (NICE) quality-adjusted life-year (QALY) threshold:

- A 9–12% increase in overall health spending

- An increase in medicine spending to >0.6% of GDP in the next 10 years

- An increase in the NICE QALY threshold to £25,000–35,000

Collectively, these changes may position the UK as a more favourable early‑launch market than other European countries.

Looking ahead, we expect increasing pressure on markets to adapt, whether through higher budgets, revised health technology assessment (HTA) thresholds, or expanded use of outcomes‑based and innovative contracting to support higher ex‑US prices while managing affordability concerns, or risk facing the threat of delayed or no launch.

Conclusions and recommendations

With 16 MFN agreements in place and mandatory MFN models progressing, manufacturers operate in a landscape defined by tightened US and ex-US price interdependence. Navigating this environment will require greater agility, stronger cross‑functional coordination and proactive scenario planning.

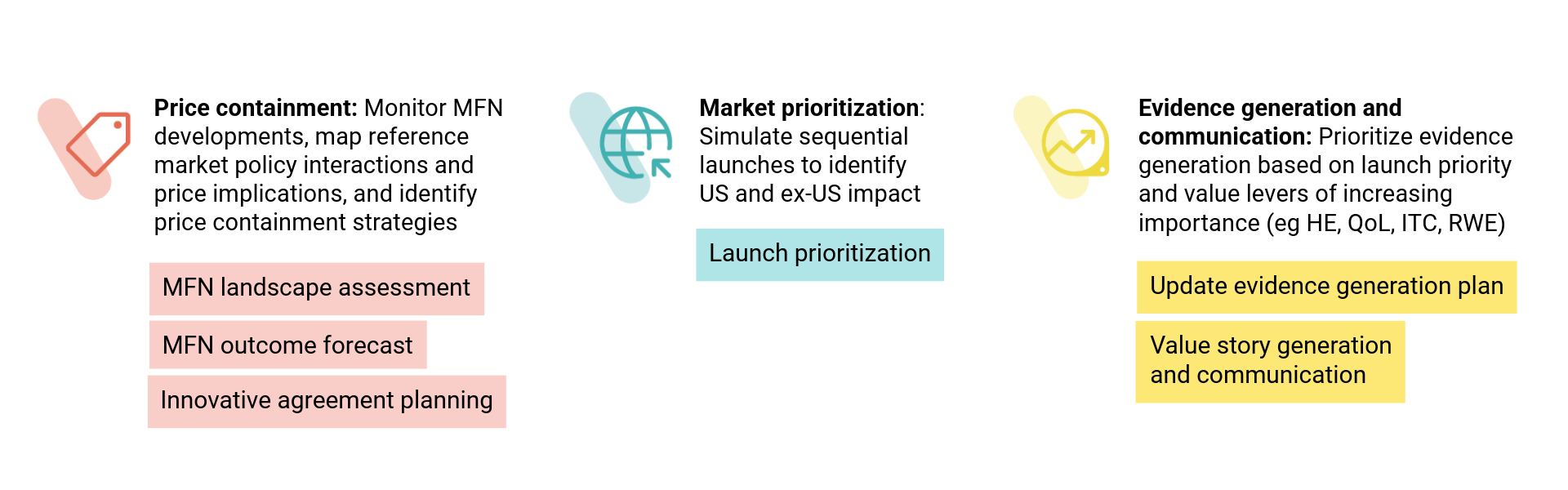

Manufacturers should not wait for full policy finalization to prepare; priority MFN‑readiness activities such as price containment, market prioritization, evidence generation and communication strategies should be initiated early (Figure 2).

Figure 2. Recommended actions for manufacturers

HE, health economics; ITC, indirect treatment comparison; MFN, most-favoured nation; QoL, quality of life; RWE, real-world evidence

If you’re preparing for MFN or need support in understanding how it could reshape your portfolio, get in touch with our team below.

About the author

Navigating the new ‘most-favoured nation’ (MFN) reality: are pharma companies ready?

Navigating the new ‘most-favoured nation’ (MFN) reality: are pharma companies ready?

Contact CTA

Start a conversation

Find out how our experts can address your healthcare communication challenges.

Navigating the new ‘most-favoured nation’ (MFN) reality: are pharma companies ready?

Subscribe to our newsletter for the latest insights

Navigating the new ‘most-favoured nation’ (MFN) reality: are pharma companies ready?

Loading posts...

No posts found.